The Chinese Social Credit System (社会信用体系, shèhuì xìnyòng tǐxì) is a broad government initiative aimed at improving “trustworthiness” across society, primarily through data collection, blacklists/redlists, and incentives or penalties.

It is not a single, unified nationwide “score” for every citizen like a dystopian Black Mirror episode (a common Western misconception), but a fragmented set of tools focused more on businesses, legal compliance, and specific behaviors than on comprehensive personal moral scoring.

Origins and Goals

The system was formalized in a 2014 State Council planning outline (2014–2020), with roots in earlier credit and regulatory efforts.

It is managed by bodies like the National Development and Reform Commission (NDRC), People’s Bank of China (PBOC), and Supreme People’s Court.

Official aims include:

- Building trust in the economy and society (e.g., reducing fraud, tax evasion, corruption, product counterfeiting).

- Enforcing compliance with laws and contracts.

- Rewarding “trustworthy” behavior and punishing “untrustworthy” actions.

- Extending to individuals, companies, government agencies, and organizations.

The government frames it as enhancing social governance where traditional laws fall short, promoting “civilized” behavior.

Key Components

It operates through several overlapping elements rather than one master algorithm:

- Financial Credit (Zhengxin System): Run by the PBOC, this is like Western credit bureaus. It tracks financial history for over a billion individuals and companies. Private scoring apps were largely curtailed by 2023.

- Blacklists and Redlists (Joint Rewards/Punishments): The most impactful part. People or companies violating laws (e.g., court judgments, serious traffic offenses, fraud) can be added to blacklists. This triggers cross-agency penalties, such as:

- Bans on buying plane/train tickets (high-speed rail).

- Restrictions on luxury purchases, loans, or certain jobs.

- Slower internet or public shaming in some cases.

- Redlists reward good behavior (e.g., charity, volunteering) with perks like discounts or priority services.

- Corporate Social Credit System (CSCS): More developed and emphasized. Tracks businesses on compliance (tax, environment, labor, IP, safety). Data is shared across agencies. Bad records can limit financing, contracts, or operations. As of recent updates (2025–2026), it includes foreign-invested firms and supports massive financing decisions.

- Local Pilots for Individuals: Some cities/counties experimented with point-based scores (e.g., starting at 1,000 points, with rules for good/bad behaviors like volunteering vs. littering or jaywalking). One analyzed “national model” used 389 rules. Many such pilots have been scaled back or ended by the mid-2020s; no unified national citizen score exists.

Current Status (as of 2025–2026)

- No nationwide personal score: Comprehensive individual scoring trials largely wound down. Focus shifted to corporate compliance and targeted enforcement.2

- Ongoing development: 2025 updates emphasized standardization, cross-ministry data sharing, and integration into economic governance. A dedicated Social Credit Law is still under discussion.

- Scale: Blacklists affect hundreds of thousands (e.g., for contract disputes). Corporate data covers millions of entities.

- Data sources: Government records, courts, police, public reports, some surveillance tech (cameras, apps), but implementation remains fragmented due to data-sharing challenges.

Common Myths vs. Reality

- Myth: Everyone has a single score dictating daily life (e.g., deducted points for jaywalking leading to total bans). Reality: Mostly blacklist-based for legal violations; everyday behavior monitoring is limited and localized.

- Myth: It’s a fully AI-driven Orwellian panopticon. Reality: Highly digitized in places but still relies on manual reporting and existing databases. It’s more regulatory enforcement tool than sci-fi surveillance.

- It does enable greater government oversight, including on political or “moral” issues in some pilots, and raises concerns about privacy, fairness, and discretionary power.

The system evolves with policy updates and reflects China’s preference for data-driven governance to maintain social order and economic reliability. For businesses operating in China, especially foreign ones, compliance with its corporate aspects is increasingly important.

Sources like Wikipedia, Stanford analyses, and official policy summaries provide the most balanced overviews.

Part 2 SCS Vs WCS

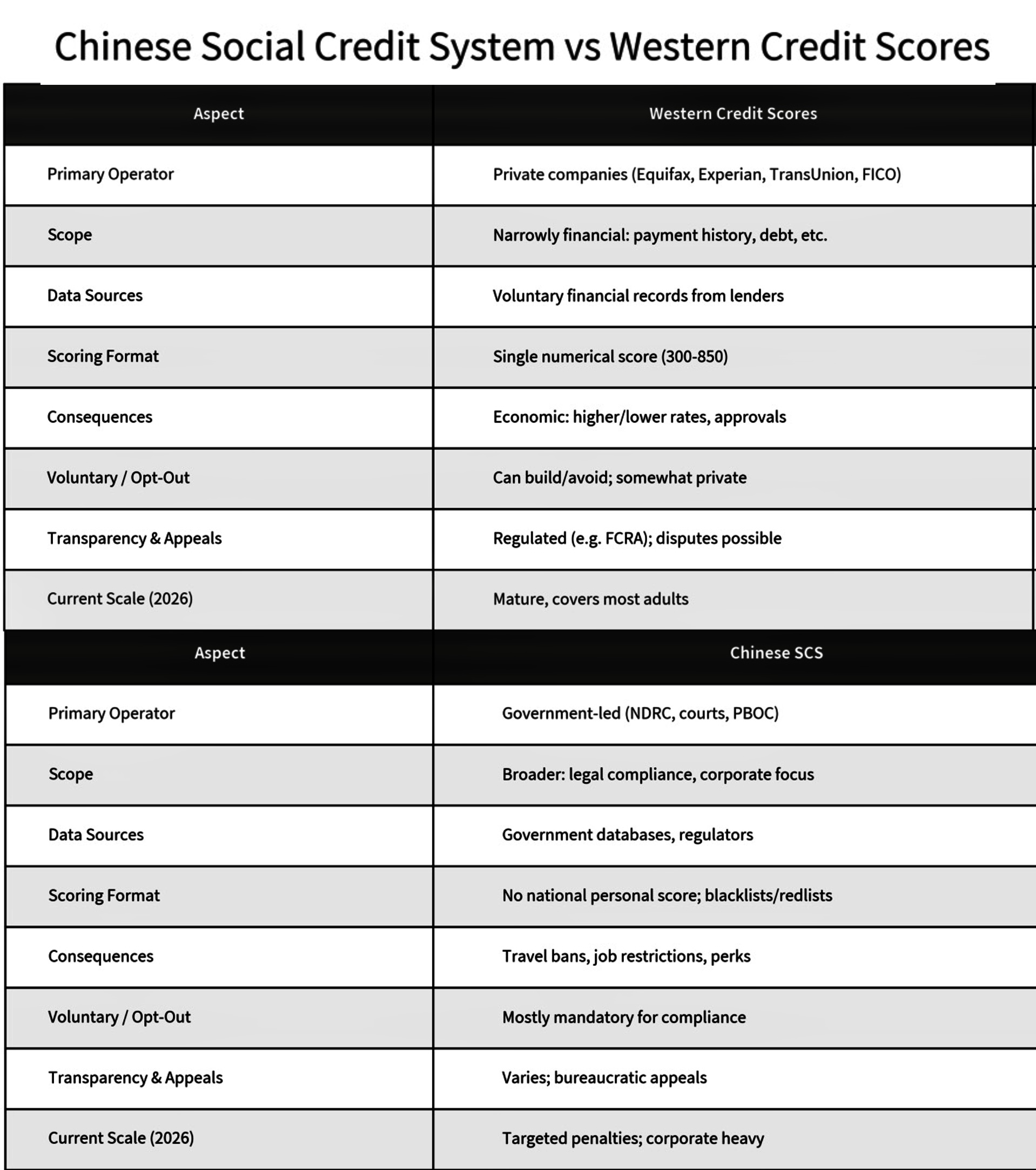

Chinese Social Credit System (SCS) vs. Western Credit Scores: A Side-by-Side Comparison

The Chinese Social Credit System and Western credit scoring (e.g., FICO or VantageScore in the US, SCHUFA in Germany, or equivalents from Experian/Equifax/TransUnion in Europe) both aim to measure “trustworthiness” to support economic activity.

However, they differ fundamentally in scope, control, data, and consequences. SCS was originally inspired by Western financial credit models in the early 2000s but evolved into a broader government tool for regulatory compliance and social governance.

As of 2026, SCS has no unified nationwide personal “citizen score” (a common myth); individual scoring pilots have largely been scaled back or ended, with the focus now on corporate compliance and targeted blacklists/redlists.

Western systems remain narrowly financial and private.

Key Similarities

- Both promote economic trust by rewarding “good” behavior (paying bills on time) and penalizing bad (defaults, fraud).

- SCS explicitly drew from FICO-style models for its financial credit foundation.

- Western systems have some “social” parallels (e.g., platform ratings on Uber/Airbnb, background checks, no-fly lists, or fintech using alternative data), but these are decentralized and not a single government system.

Key Differences & Nuances

- Government vs. Private Control: Western scores are market-driven and regulated for consumer protection. SCS is a state tool for broader governance (enforcing laws, reducing corruption/fraud), which critics argue enables greater oversight.

- Not a Dystopian Single Score: Media often portrays SCS as an omnipresent AI “citizen score” deducting points for jaywalking or politics. In reality, it’s fragmented, mostly blacklist-based for serious violations, and far more focused on businesses than everyday personal life.

- Real-World Impact: Western scores affect your wallet. SCS blacklists can restrict mobility and opportunities in tangible ways (e.g., travel bans for unpaid court fines).

In short, Western credit is a financial reputation tool run by the market.

SCS is a comprehensive regulatory and compliance framework run by the state—broader in ambition but more targeted in current practice.

Both have strengths (encouraging reliability) and risks (bias, errors, overreach).

For businesses in China, the corporate SCS is increasingly relevant for operations and financing.